HDD Prices 2020-2026: How AI Data Centers Triggered a 46% Price Surge

Quick Answer+

HDD Price Summary 2020-2026: The hard disk drive market is experiencing its most dramatic price surge in over a decade. Since September 2025, HDD prices have increased by an average of 46%, with some models up 66%. The Seagate BarraCuda 24TB now costs $499 (was $239), and the Seagate IronWolf 8TB jumped from $130 to $199. Both Western Digital and Seagate have their entire 2026 production sold out. Supply relief is not expected before 2027 at the earliest.

For decades, hard drive pricing followed a predictable trajectory: steadily downward. Then AI changed everything. The insatiable appetite of hyperscale data centers for mass-capacity storage has fundamentally altered the HDD market, creating what Seagate’s Chief Commercial Officer Ban-Seng Teh calls “the new normal.”

This comprehensive analysis examines HDD price trends from 2020 through early 2026, explains the driving forces behind the current 46% price surge, and offers forecasts for consumer and enterprise buyers planning storage investments through 2027.

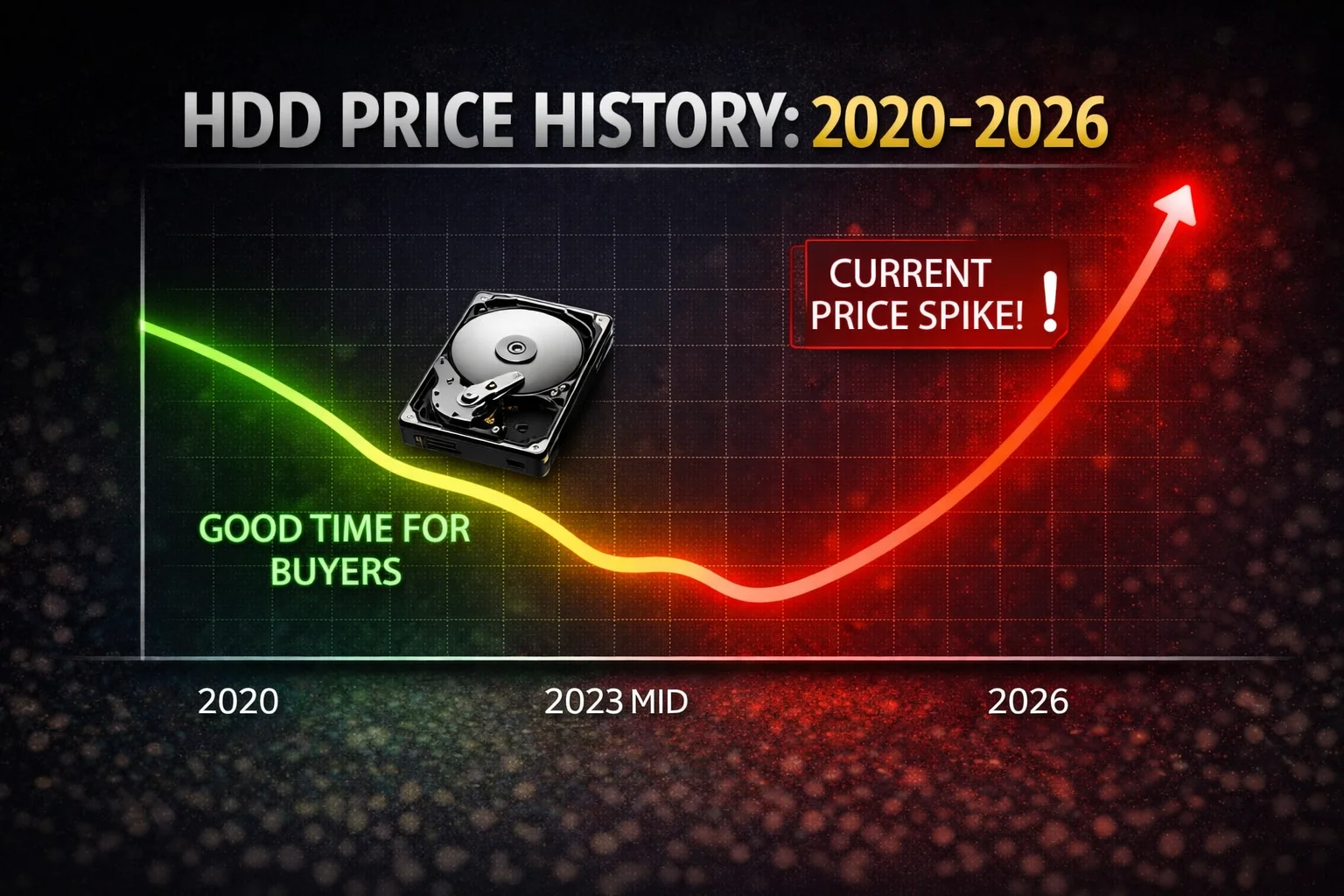

HDD Price History: 2020-2026 Overview Chart

The following chart illustrates the average consumer HDD price per terabyte from January 2020 through February 2026:

📊 Average Consumer HDD Price ($/TB) — 2020-2026

Sources: Backblaze, TrendForce, Tom’s Hardware, Amazon/Newegg retail tracking. Data represents average consumer HDD prices.

Historical Context: The Long Decline (2009-2024)

For decades, hard drive pricing followed a predictable trajectory: steadily downward. According to Backblaze’s comprehensive analysis of drive costs, the average price per gigabyte dropped from $0.114 in 2009 to just $0.014 by November 2022 — an 87.4% decrease over 13 years.

The Thailand Floods: A Cautionary Parallel

The most significant disruption to HDD pricing prior to 2025 occurred in October 2011, when devastating floods in Thailand submerged factories responsible for nearly 50% of worldwide hard drive manufacturing capacity. Thailand was — and remains — the world’s second-largest producer of hard disk drives, supplying approximately 25% of global production.

The impact was immediate and severe. Backblaze, the cloud storage provider that publishes detailed drive statistics, documented drive prices nearly tripling overnight. A 3TB Hitachi drive that sold for $129 just two weeks earlier suddenly cost $349. The Seagate Barracuda XT 3TB saw prices spike 138%, from $179.99 to $429.99. A typical 1TB HDD jumped from $60 to $160.

| Drive Model | Pre-Flood | Post-Flood | Increase | % |

|---|---|---|---|---|

| Seagate Barracuda XT 3TB | $179.99 | $429.99 | +$250 | 138% |

| Hitachi Deskstar 7K3000 3TB | $129.00 | $349.00 | +$220 | 170% |

| WD Scorpio Black 750GB | $89.00 | $227.00 | +$138 | 155% |

| Generic 1TB HDD | $60.00 | $160.00 | +$100 | 167% |

Source: TechSpot, Backblaze, Newegg historical pricing data

The critical difference between 2011 and 2025 is the nature of the disruption. The Thailand floods were a supply shock — a temporary disaster that disrupted manufacturing capacity. Once factories recovered (Western Digital resumed production within 46 days), prices gradually normalized, though the industry consolidated significantly in the aftermath.

Today’s surge is fundamentally different: it is demand-driven, with both major manufacturers (Seagate and Western Digital) operating at full capacity yet still unable to meet orders. This structural shift has far more lasting implications for pricing.

The 2025-2026 Price Surge: Anatomy of a Crisis

Timeline of Events

The current HDD pricing crisis did not emerge overnight. It developed through a series of escalating market pressures:

| Date | Event |

|---|---|

| Q2 2024 | HDD demand begins recovering after hyperscaler inventory digestion period; 42% YoY increase in nearline drive shipments |

| Apr 2024 | Western Digital notifies partners of 5-10% price increase due to supply constraints |

| Sep 2025 | Western Digital announces 10% across-the-board price hike; Seagate follows days later |

| Q4 2025 | Contract negotiations conclude with 4% QoQ price increase — largest in eight quarters (DigiTimes/TrendForce) |

| Nov 2025 | Seagate ships over 1 million HAMR drives; announces capacity committed through 2026 |

| Dec 2025 | Consumer prices surge; 24TB Seagate BarraCuda reaches $499 (was $239 during Black Friday 2025) |

| Jan 2026 | Average HDD prices up 46% from September; some models up 66% (Tom’s Hardware analysis) |

| Feb 2026 | Western Digital confirms 100% of 2026 production sold out; supply agreements extend through 2028 |

Sources: DigiTimes, TrendForce, Tom’s Hardware, company earnings calls

Current Retail Price Analysis

The impact on consumer pricing has been severe. Tom’s Hardware documented that the Seagate IronWolf 4TB, which sold for $70 in early 2023, now costs $99 — a 41% increase. The 8TB model jumped from $130 to $199, representing a 53% increase. Western Digital’s Red Plus 8TB alternative is now priced at $175.

Perhaps most dramatically, the Seagate BarraCuda 24TB — a popular consumer drive that regularly sold for as little as $239 during sales events — now commands $499 on Amazon, and often only through third-party sellers. At Newegg, it frequently shows as out of stock entirely.

| Drive | 2023 Price | Q1 2026 | Change | % Inc. |

|---|---|---|---|---|

| Seagate IronWolf 4TB | $70 | $99 | +$29 | 41% |

| Seagate IronWolf 8TB | $130 | $199 | +$69 | 53% |

| WD Red Plus 8TB | $120 | $175 | +$55 | 46% |

| Seagate BarraCuda 24TB | $239* | $499 | +$260 | 109% |

| Seagate Exos 20TB (Enterprise) | $299 | $449 | +$150 | 50% |

*Black Friday 2025 sale price. Regular pricing was higher. Sources: Amazon, Newegg, Tom’s Hardware

The AI Factor: Why Data Centers Are Consuming the World’s HDDs

The primary driver of the current HDD shortage is the explosive growth of AI infrastructure. Major tech companies are projected to spend over $600 billion on hyperscale data center expansion in 2026 alone — a 36% increase over 2025. Roughly 75% of this spend ($450 billion) is directly tied to AI infrastructure.

The Hyperscale Storage Demand Explosion

According to the Synergy Research Group, operational hyperscale data centers reached 1,297 facilities worldwide by late 2025 — nearly triple the number from early 2018. These facilities now account for 44% of worldwide data center capacity, a figure expected to reach 61% by 2030.

The data these facilities must store is growing exponentially. IDC forecasts global data volume will reach 181 zettabytes by the end of 2025, with projections exceeding 394 zettabytes by 2028. To put this in perspective, a single zettabyte equals one trillion gigabytes — enough to store 250 billion DVDs.

Why AI Needs HDDs, Not Just SSDs

Despite the speed advantages of solid-state drives, HDDs remain the dominant storage medium for cloud data centers. According to IDC, approximately 89% of data stored by leading cloud service providers resides on HDDs.

The reason is economics. SSDs currently cost 16 times more per terabyte than HDDs for data center applications. VDURA’s analysis revealed that enterprise SSD pricing increased by 257% between Q2 2025 and Q1 2026, while HDD pricing rose ‘only’ 35% in the same timeframe. The cost gap between SSD and HDD capacity went from 6.2x in Q2 2025 to 16.4x in Q1 2026.

AI workloads have a specific storage hierarchy that favors HDDs for the bulk of data:

| Data Tier | Use Case | Storage Medium | Data Volume |

|---|---|---|---|

| Hot | Active training, inference | NVMe SSD, HBM | ~5% of total |

| Warm | Pre-processing, staging | QLC SSD | ~10% of total |

| Cold | Training datasets, archives | Nearline HDD | ~85% of total |

Source: Seagate, Dell’Oro Group, TrendForce analysis

As Dell’Oro Group analyst Baron Fung explains: “For storing massive amounts of unstructured, raw data, cold storage on HDDs makes more sense. SSDs make sense for warm storage, such as for pre-processing data and for post-training and inference.”

Manufacturer Response: Sold Out Through 2026

Seagate: HAMR Technology and Record Margins

Seagate has emerged as the clear technology leader in this cycle. The company’s Heat-Assisted Magnetic Recording (HAMR) technology — which uses a laser to briefly heat the disk surface during writing, enabling higher data density — has achieved volume production with its Mozaic 3+ platform, delivering 3TB+ per disk platter.

Seagate has shipped over 1 million HAMR drives and delivered 550 exabytes of capacity in the past year. The company’s roadmap projects 40TB drives by late 2026, 50TB by 2027, and a path to 100TB+ drives by 2032.

According to CEO Dave Mosley at the company’s Q1 2026 earnings call, nearly 80% of nearline volume is now at or above 24TB per drive, with an expected 50% exabyte crossover to HAMR drives in 2026. Seagate’s nearline capacity is on allocation through the end of 2026, with supply agreements extending into 2027.

Western Digital: 100% Sold Out

Western Digital’s situation is equally constrained. The company announced that its entire 2026 HDD production capacity is 100% sold out, with long-term supply agreements extending through 2028. Hyperscaler AI cloud customers now account for 89% of Western Digital’s HDD revenue, with consumer products representing just 5%.

Western Digital lags Seagate in HAMR adoption, with its first 36TB HAMR drive not expected until at least 2027 — a 12-18 month technology gap. However, the company’s shares have still surged 489% between March 2025 and March 2026, rising from $44 to $259, driven by strong revenue growth and expanding profit margins.

Why Manufacturers Won’t Expand Capacity

Despite record demand, neither Seagate nor Western Digital has announced plans to significantly expand production capacity. This is a deliberate strategy born from painful experience.

Seagate’s CEO stated that the company hopes to “take advantage of this demand environment to maximize profits by controlling supply and optimizing its product mix.” The company is increasing investment in data center and enterprise-grade products while essentially telling consumers who find products too expensive to “look elsewhere.”

This approach reflects lessons learned from the industry’s boom-bust cycles. From 2020 to 2025, consumer-grade HDD revenue share at both companies declined from over 20% to less than 10%. The enterprise segment, which offers higher margins and longer-term contracts, is now the priority.

Secondary Factors Driving the Shortage

China’s PC Market Resurgence

A surprising secondary driver has emerged from China’s PC market. Government procurement policies now favor domestically produced CPUs and operating systems, which has accelerated local PC production.

Intriguingly, this policy shift has also boosted HDD adoption due to concerns about SSD data retention. NAND flash memory in SSDs is vulnerable to ‘bit rot’ — data deterioration over time when stored without power. For government and enterprise applications requiring long-term data integrity, HDDs remain the preferred medium.

The DRAM Squeeze

HDDs utilize DRAM for cache memory, and the ongoing DRAM shortage has complicated the supply situation. Server DRAM contract prices were forecast to surge 90% quarter-over-quarter in Q1 2026 — the steepest single-quarter increase on record. PC DRAM prices are expected to more than double in the same period.

As Seagate’s CCO Ban-Seng Teh told the South China Morning Post: “It’s hard to tell if it will last forever. The current cycle is very unusual because in the past we went through cycles of shortage and oversupply.” The company had “definitely seen increasing costs” due to rising DRAM prices.

Supply Chain and Logistics Pressures

Additional pressures include rising freight costs (up 30% since 2024), port delays in Asia, and geopolitical factors including U.S.-China tariff tensions. The Biden administration expanded import tariffs on semiconductors from China to 50%, and while many suppliers manufacture outside China, these tariffs tighten an already pressured market.

Forecast: What to Expect Through 2027

Short-Term Outlook (2026)

Supply relief is not expected before 2027 at the earliest. Both major manufacturers have their capacity fully committed through calendar year 2026, with long-term agreements providing visibility through 2027-2028.

Industry analysts project an additional 10-18% price increase for enterprise HDDs through Q1 2026, with consumer prices likely following. The ‘HDD Sold-out’ condition is systemic, with nearline capacity fully allocated.

For consumers, this means expecting to pay $50+ more per drive compared to late 2024 pricing. Manufacturers are prioritizing high-margin enterprise customers, leaving consumer products with longer lead times, higher list prices, and fewer alternatives.

Medium-Term Outlook (2027-2028)

By 2027, HAMR technology should be fully ramped at both manufacturers, enabling higher-capacity drives (40-50TB) at improved economics. Seagate’s 40TB HAMR drives, expected in mid-2026, promise to dramatically expand gross margins as they slash the company’s production cost per terabyte.

However, demand growth may continue to outpace supply. Analyst Tom Coughlin predicts HDD capacity shipments will reach approximately 7.3 zettabytes by 2029, with nearline HDDs comprising over 90% of shipments (compared to 54% today).

Price Forecast Summary

| Segment | 2026 | 2027 | Outlook |

|---|---|---|---|

| Consumer NAS (4-8TB) | +10-15% | Stable to -5% | Gradual relief |

| High-Cap Consumer (16-24TB) | +15-25% | +5-10% | Elevated |

| Enterprise Nearline | +10-18% | +5-10% | Premium persists |

| External/Portable | +5-10% | Stable | Moderate impact |

Source: StorageDiskPrices.com analysis based on industry data from TrendForce, IDC, and manufacturer guidance

Recommendations for Buyers

For Consumer and Prosumer Buyers

- Buy now if you need capacity: If you’ve been waiting for prices to return to 2024 levels, that wait may extend well into 2027. Current pricing, while elevated, may represent a relative value compared to later 2026.

- Consider refurbished enterprise drives: Data center decommissioned drives often offer excellent value. Look for certified refurbished Seagate Exos or WD Ultrastar drives with remaining warranty.

- Monitor external drive deals: External drives sometimes offer better value than internal drives of equivalent capacity. ‘Shucking’ (removing internal drives from external enclosures) remains a valid strategy for budget-conscious buyers.

- Check our Price Per TB page: Find the current best value drives across all capacities.

For Small Business and IT Buyers

- Lock in contracts early: If your business has predictable storage needs, consider pre-order contracts with 90-day price guarantees through authorized distributors.

- Implement hybrid storage architectures: Pair high-capacity HDDs for cold storage with smaller SSDs for hot data. This approach can reduce total storage costs by 27-37% compared to all-SSD deployments.

- Plan lead times carefully: Current enterprise HDD deliveries are taking 6-8 weeks or longer. Plan replenishment 3 months ahead, not 3 weeks.

Best Value HDDs in the Current Market

Key Takeaways

- 46% average price surge: HDD prices have risen sharply since September 2025, with some models up 66%

- AI changed everything: Hyperscale data centers are the primary demand driver, not consumers

- Both manufacturers sold out: Seagate and Western Digital have 2026 capacity fully committed

- Supply relief is years away: New capacity won’t ease shortages until 2027 at the earliest

- HDDs are critical infrastructure: 89% of cloud data still resides on HDDs — they’re far from obsolete

- Buy what you need now: Waiting is unlikely to save money in this market environment

Frequently Asked Questions

HDD prices are rising primarily due to AI data center demand consuming unprecedented quantities of nearline storage. Both Seagate and Western Digital have their entire 2026 production capacity sold out, with hyperscaler cloud customers accounting for 89% of HDD revenue. Additionally, DRAM shortages are increasing component costs, and manufacturers are deliberately prioritizing high-margin enterprise products over consumer drives.

Industry analysts don’t expect meaningful price relief until late 2027 or 2028 when HAMR technology is fully ramped at both manufacturers and new higher-capacity drives (40-50TB) improve per-terabyte economics. However, demand growth from AI infrastructure may continue to outpace supply, meaning pre-2025 pricing levels may not return.

Since September 2025, average HDD prices have increased by 46% according to Tom’s Hardware analysis. Some individual models have seen increases as high as 66%. The Seagate BarraCuda 24TB went from $239 to $499 (109% increase), and the Seagate IronWolf 8TB rose from $130 to $199 (53% increase).

Buy now if you need storage. Both major manufacturers are sold out through 2026, and prices are expected to continue rising through at least Q2 2026. Waiting is unlikely to save money. The only exception is if you can wait until late 2027 when HAMR technology improvements and potential capacity expansion may provide some relief.

No — this is fundamentally different. The 2011 Thailand floods were a supply shock that temporarily disrupted manufacturing. Factories recovered within weeks and prices normalized. The current surge is demand-driven — both manufacturers are operating at full capacity but still can’t meet orders from AI data centers. This structural shift has far more lasting implications for pricing.

Economics. SSDs cost 16 times more per terabyte than HDDs for data center applications. Approximately 85% of AI workload data (training datasets, archives) resides in ‘cold storage’ where HDD performance is adequate. SSDs are reserved for the ~5% of data that needs high-speed access during active training and inference. IDC reports that 89% of data at leading cloud providers is stored on HDDs.

HAMR (Heat-Assisted Magnetic Recording) is Seagate’s breakthrough technology that uses a tiny laser to briefly heat the disk surface during writing, enabling much higher data density per platter — currently 3TB+ per platter. Seagate has shipped over 1 million HAMR drives and projects 40TB drives by late 2026, 50TB by 2027, and 100TB+ by 2032. This technology is key to improving per-terabyte economics over time.

Currently, 8-12TB drives tend to offer the best balance of price per terabyte and availability. High-capacity drives (16TB+) have experienced the steepest increases due to enterprise demand. External drives sometimes offer better value than internal drives — ‘shucking’ (removing the drive from an external enclosure) remains a viable strategy. Check our Price Per TB page for current best values.

Data Sources and Methodology

This analysis draws from multiple authoritative sources:

- TrendForce: Quarterly storage reports and NAND/HDD market forecasts

- IDC: Global DataSphere forecasts and market analysis

- Seagate and Western Digital: Earnings calls and investor presentations

- DigiTimes Asia: Market intelligence and supply chain reporting

- Backblaze: Drive statistics and pricing analysis

- Tom’s Hardware: Market analysis, Network World, and industry trade publications

- Retail pricing: Amazon, Newegg, and diskprices.com

Consumer HDD prices represent averages across internal desktop and NAS drives. Enterprise nearline pricing is tracked separately due to different market dynamics and contract structures.

Related Storage Guides

- SSD Price History 2020-2026 — Complete SSD price analysis and forecast

- Best Drives for Data Hoarding — Maximum storage solutions

- Best NAS Drives 2026 — Top picks for network storage

- SSD vs HDD — When each makes sense in 2026

- CMR vs SMR — HDD recording technology explained

- Price Per TB Calculator — Find the best value drives

- Seagate IronWolf Guide — Complete IronWolf lineup

- WD Red Plus Guide — Complete Red Plus lineup

- Seagate Exos Guide — Enterprise drive breakdown

- Best External Hard Drives — Portable and desktop options

- How Much Storage Do I Need? — Capacity planning guide

Last Updated: March 2026 | Data verified from TrendForce, IDC, Backblaze, and market tracking sources