From $50 to $150: What Happened to Cheap SSDs?

From $50 to $150: What Happened to Cheap SSDs?

If you bought an SSD in 2023, congratulations—you timed the market perfectly. If you’re shopping for one now in February 2026, prepare for sticker shock. That 1TB NVMe drive that cost $50 during the 2023 price collapse? It’s now $150 or more. The same Samsung 990 Pro that hit $99 on sale is now retailing for $218. What happened to the era of cheap SSDs? The short answer is AI. The longer answer involves a perfect storm of artificial intelligence infrastructure demand, strategic manufacturing decisions, and a fundamental restructuring of the global memory industry that may keep prices elevated for years.

The Golden Era We Didn’t Know We Had (2022-2023)

To understand how dramatic the current situation is, we need to look back at what storage enthusiasts now call “the golden era” of SSD pricing.

In 2022 and 2023, SSD prices crashed to unprecedented lows. The COVID-19 pandemic had triggered a massive surge in PC and laptop demand as millions shifted to remote work. Memory manufacturers responded by ramping up production—only to see demand normalize faster than expected. The result was a classic oversupply situation.

The 2023 Price Floor

By mid-2023, consumer SSD prices hit all-time lows:

- 1TB NVMe drives: As low as $45-50 (5 cents per GB)

- 2TB NVMe drives: Under $100

- 4TB NVMe drives: Around $200

- Samsung 990 Pro 1TB: $99 on sale

- WD Black SN770 1TB: $50-60

- Crucial MX500 1TB: $55

Tech enthusiasts were building massive storage arrays. Data hoarders were filling multi-terabyte NAS systems with affordable SSDs. The consensus was that SSD prices would continue falling, eventually reaching parity with HDDs. “Wait for lower prices” was common advice.

That advice turned out to be catastrophically wrong.

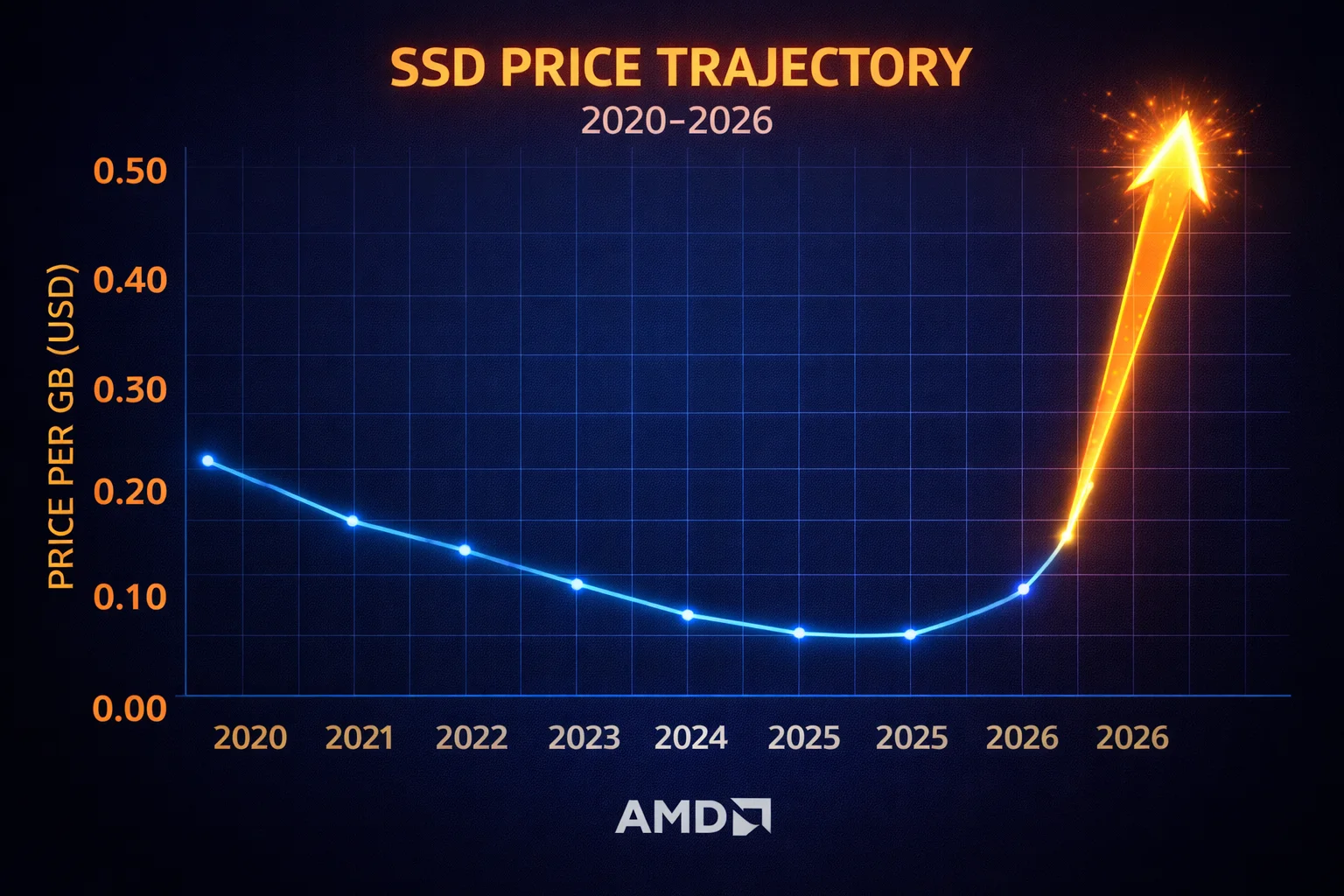

SSD Price History: The Complete Timeline

Here’s what happened to consumer SSD prices from 2020 through February 2026:

Consumer SSD Price Per GB (2020-2026)

| Period | Avg $/GB | 1TB NVMe Price | Key Events |

|---|---|---|---|

| Early 2020 | $0.12 | $120-140 | COVID begins, demand surges |

| Q2 2021 | $0.14 | $140-160 | Peak COVID premium, supply chain chaos |

| 2022 | $0.09 | $90-110 | Oversupply begins, prices falling |

| Mid-2023 | $0.05 | $45-55 | ALL-TIME LOW – Golden Era |

| 2024 | $0.065 | $65-75 | AI demand emerges, production cuts |

| Q4 2025 | $0.10 | $100-120 | NAND shortage intensifies |

| Q1 2026 | $0.13+ | $130-160+ | Crisis mode – 200%+ from 2023 |

The numbers are stark: A 1TB SSD that cost $50 in mid-2023 now costs $130-150—a 160-200% increase in just 2.5 years.

What Happened? The Five Forces Behind the Price Explosion

The SSD price crisis isn’t caused by a single factor—it’s a convergence of five major forces that together created what industry analysts are calling a “perfect storm.”

1. AI Data Centers Are Devouring Global Memory Production

This is the primary driver. The explosion of generative AI—ChatGPT, Claude, Midjourney, and enterprise AI deployments—requires astronomical amounts of memory and storage. Every AI model, from consumer chatbots to industrial language models, needs massive NAND flash capacity for training data, model weights, and inference caching.

The numbers are staggering:

In October 2025, OpenAI formally announced a partnership with Samsung and SK Hynix for its “Stargate” AI infrastructure project. The deal requires up to 900,000 DRAM wafers per month—approximately 40% of the entire world’s DRAM production. This single project is large enough to create shortages across the entire consumer market.

But it’s not just OpenAI. Every major tech company is racing to build AI infrastructure. Microsoft, Google, Meta, Amazon, and dozens of others are all competing for the same limited supply of memory chips.

2. HBM Is Eating Your SSD’s Lunch

High Bandwidth Memory (HBM) is the specialized memory used in AI accelerators like Nvidia’s H100 and B200 GPUs. HBM is critical for AI workloads because it provides massive bandwidth for moving data in and out of processors.

The problem? HBM consumes approximately 3x the wafer capacity per gigabyte compared to standard DRAM or NAND. When memory manufacturers allocate a wafer to HBM production, that’s three times fewer consumer memory chips produced.

Memory Manufacturing Priority Shift (2023 vs 2026)

Priority

Priority

Source: Industry analyst estimates based on manufacturer disclosures

SK Hynix now controls over 50% of the global HBM market, with Samsung at roughly 35% and Micron at 11%. All three are prioritizing HBM production because the margins are extraordinary—SK Hynix reportedly secured a 50% price premium for HBM4 over HBM3E in its Nvidia deals.

3. Memory Manufacturers Learned Their Lesson (The Hard Way)

In 2022-2023, memory manufacturers were caught with massive oversupply. Samsung, SK Hynix, and Micron all suffered significant financial losses as prices crashed below production costs. Samsung actually cut production of 3D NAND and DRAM to stop the bleeding.

The three memory giants—which together control approximately 95% of global DRAM production—have learned to be cautious about expanding capacity. They’re now exercising what the industry calls “supply discipline”:

- Samsung: Prioritizing HBM4 and high-margin enterprise products

- SK Hynix: Production capacity sold out through 2026

- Micron: Exited the consumer memory market entirely in December 2025

Yes, you read that correctly. Micron—the company behind the Crucial brand—announced it’s exiting the consumer memory market to focus entirely on enterprise and AI customers. When asked, executives stated that “winding down Crucial would free up wafer supply for strategic accounts.”

This is a structural shift, not a temporary fluctuation. Memory manufacturers have decided that consumer products aren’t worth the wafer capacity.

4. New Fabs Take Years to Build

Building a new semiconductor fabrication facility isn’t like opening a new factory. Modern memory fabs are among the most complex manufacturing facilities on Earth, costing $10-20 billion and taking 3-5 years to bring online.

Current expansion plans won’t provide relief until 2027 at the earliest:

| Manufacturer | Facility | Expected Online | Priority |

|---|---|---|---|

| Micron | Hiroshima HBM Fab | 2028 | HBM |

| Samsung | P5 Pyeongtaek | 2028 | HBM/Enterprise |

| SK Hynix | M15X Facility | Mid-2027 | HBM/DRAM |

| Micron | ID1 Fab (US) | 2027 | DRAM |

Even when these facilities come online, company executives have stated that HBM and high-margin enterprise DRAM will receive priority through at least 2027.

5. The Supply Chain Is Cannibalizing Itself

HDD shortages have created a secondary effect that’s worsening the SSD situation. Enterprise customers who can’t get nearline HDDs (which are backordered 52+ weeks) are switching to SSDs instead, further straining NAND supply.

Meanwhile, the graphics memory market is also affected. The transition to GDDR7 for next-generation GPUs created GDDR6 shortages, inflating those prices by around 30%. GPU manufacturers face the same capacity constraints as everyone else.

This creates what industry analysts call a “cascade effect”—shortages in one segment drive demand into other segments, which then become short, driving demand elsewhere. The entire storage hierarchy is being rewritten.

The Human Impact: What Real Prices Look Like Now

Let’s look at concrete examples of popular SSDs and how their prices have changed:

Popular 1TB NVMe SSD Prices: Then vs Now

Prices based on major retailer listings. Sale prices during 2023 golden era vs current February 2026 retail.

The Crucial MX500’s 254% increase is particularly notable because Micron (Crucial’s parent company) has announced it’s exiting the consumer market entirely. Remaining inventory is being sold at premium prices.

Enterprise SSDs: Even Worse

If you think consumer prices are bad, enterprise customers are experiencing even steeper increases. According to VDURA’s analysis, between Q2 2025 and Q1 2026:

- 30TB TLC enterprise SSD: $3,062 → $11,000 (257% increase)

- SSD-to-HDD cost ratio: 6.2x → 16.4x

- Enterprise SSD contract prices: 15-20% increases per quarter

Dell Technologies COO Jeff Clarke stated during a November 2025 analyst call that the company had “never witnessed costs escalating at the current pace.” Morgan Stanley subsequently downgraded Dell stock, citing the company’s exposure to rising memory costs.

The Global Response: Rationing Has Begun

The shortage has become severe enough that some retailers are implementing purchase limits—something unprecedented for the consumer storage market.

Japanese PC retailers have begun limiting SSD, HDD, and RAM purchases to prevent hoarding. Some shops now restrict customers to one or two storage drives per transaction. Framework, the modular laptop manufacturer, delisted standalone memory modules to “head off scalpers and preserve inventory.”

Even Raspberry Pi—makers of some of the world’s cheapest computers—raised prices in October 2025, citing memory costs that are “roughly 120% more than a year ago.”

What Industry Executives Are Saying

The warnings from industry leaders have become increasingly dire:

“Every NAND manufacturer told us 2026 sold out. All the capacity sold out.”

— Khein-Seng Pua, CEO of Phison, November 2025

“It’s bad, and it’s getting worse right now. NAND prices increased by 246% from Q1 2025, 70% of that happening in just the last 60 days.”

— Cameron Crandall, Kingston Datacenter SSD Business Manager, December 2025

“We have never witnessed costs escalating at the current pace.”

— Jeff Clarke, COO of Dell Technologies, November 2025

“Memory inventories are approximately 50% above normal levels in anticipation of further price increases.”

— Winston Cheng, CFO of Lenovo

When Will Prices Drop? The Uncomfortable Truth

Here’s the difficult reality: prices are unlikely to return to 2023 levels anytime soon—possibly ever.

This isn’t a cyclical shortage that will naturally correct. It’s a structural reallocation of manufacturing capacity. For decades, consumer DRAM and NAND production was the primary driver for memory manufacturing. Today, that dynamic has inverted. AI infrastructure is now the priority, and consumers are an afterthought.

The Timeline for Any Relief

| Period | Expected Situation | Price Outlook |

|---|---|---|

| Q1-Q2 2026 | Peak shortage, inventory depletion | ↑ 20-40% additional increases |

| Q3-Q4 2026 | Structural high baseline stabilization | → Prices plateau at elevated levels |

| 2027 | New fab capacity begins coming online | → Possible modest relief |

| 2028+ | Significant new capacity operational | ↓ Gradual improvement possible |

Some analysts warn that NAND shortages could persist for the rest of the decade, depending on AI adoption curves. The memory supercycle some are predicting could last through 2030.

IDC’s analysis is particularly sobering: “This is not just a cyclical shortage driven by a mismatch in supply and demand, but a potentially permanent, strategic reallocation of the world’s silicon wafer capacity.”

SSD vs HDD: The Gap Is Growing Again

For years, the SSD-to-HDD price gap was narrowing. Many predicted SSDs would eventually reach price parity with hard drives. The 2025-2026 shortage has reversed that trend dramatically.

Cost Per TB: SSD vs HDD (2023-2026)

As of February 2026, SSDs cost approximately 7-8x more per TB than HDDs—the widest gap since 2019. For bulk storage applications, this makes HDDs attractive again for those who can tolerate the noise and slower performance.

However, HDDs are also experiencing shortages. Enterprise nearline drives are backordered 52+ weeks at major manufacturers. Western Digital raised HDD prices 5-10% in 2024, and further increases are expected.

What Should You Do? Practical Advice

If You Need an SSD Now

Don’t wait. Prices are rising, not falling. Every forecast suggests Q1-Q2 2026 will see additional 20-40% increases. The drive that costs $130 today may cost $180 in three months.

Buy what you need, but don’t hoard. Hoarding contributes to shortages and may trigger purchase limits at retailers.

Consider 4TB drives. Larger capacity drives currently offer better $/TB value because enterprise demand focuses on maximum capacity, leaving mid-range consumer drives relatively better supplied.

If You Can Wait

Target late 2027. That’s when significant new fab capacity should begin easing shortages—but even then, prices may not return to 2023 levels.

Monitor Chinese suppliers. CXMT (ChangXin Memory Technologies) is preparing a $4.2 billion USD IPO to expand domestic Chinese memory production. This could eventually provide alternative supply.

Consider Alternative Strategies

Hybrid storage: Use a smaller SSD for OS and frequently accessed files, with HDD for bulk storage. Our guides on IronWolf HDDs and NAS compatibility can help you build efficient hybrid systems.

QLC for bulk storage: Despite lower endurance, QLC SSDs are more available and offer better $/TB for archival use cases.

NAS with HDD arrays: For large storage needs, a NAS with 12TB or 16TB HDDs offers far better $/TB than SSDs, even accounting for the NAS hardware cost.

The Bigger Picture: AI Changed Everything

What we’re witnessing isn’t just a memory shortage—it’s a fundamental restructuring of the semiconductor industry’s priorities. For decades, consumer electronics drove memory demand. Smartphones, PCs, and laptops were the primary customers for DRAM and NAND.

That era is over.

AI infrastructure is now the primary driver. A 2024 McKinsey analysis projected that AI workloads will consume roughly 70% of total data center capacity by 2030. The voracious demand for HBM from hyperscalers like Microsoft, Google, Meta, and Amazon has forced memory manufacturers to pivot their limited cleanroom space and capital expenditure toward higher-margin enterprise-grade components.

This is a zero-sum game. Every wafer allocated to an HBM stack for an Nvidia GPU is a wafer denied to the consumer SSD you want to buy.

As IDC bluntly stated: “This signals the end of an era of cheap, abundant memory and storage, at least in the medium term.”

A Note on the “AI Bubble” Argument

Some hope that an AI bubble burst could restore normalcy to memory markets. This argument has merit—if AI investment slows dramatically, demand for HBM and enterprise storage would decrease, potentially freeing capacity for consumer products.

However, memory manufacturers have learned from 2022-2023. They’re now coordinating to prevent memory hoarding, which should stabilize demand even if AI investment contracts. Samsung, SK Hynix, and Micron have explicitly stated they won’t aggressively expand production to avoid another oversupply situation.

Even in a bubble-burst scenario, the path back to $50 1TB SSDs would be long and uncertain.

Conclusion: The New Normal

The era of cheap SSDs that began in 2022 and peaked in mid-2023 was an anomaly—a market correction that briefly made solid-state storage accessible at prices approaching hard drives. That window has closed.

What we’re experiencing now isn’t temporary inflation. It’s a structural shift in how the memory industry allocates its limited production capacity. AI infrastructure has become the priority customer, and consumer products are receiving whatever capacity remains after enterprise demands are met.

The numbers tell the story: a 1TB SSD that cost $50 in mid-2023 now costs $130-150, with further increases expected. New fab capacity won’t provide meaningful relief until 2027-2028 at the earliest. Micron has exited the consumer market entirely. Japanese retailers are rationing purchases.

This is the new normal. Plan your storage purchases accordingly.

Frequently Asked Questions

SSD prices have increased 200%+ from 2023 lows due to AI data center demand consuming global NAND production, manufacturers prioritizing high-margin HBM over consumer products, all 2026 production capacity being sold out, and Micron exiting the consumer market. This is a structural shift, not a temporary fluctuation.

Meaningful price relief isn’t expected until late 2027 at the earliest, when new fab capacity comes online. However, industry analysts warn prices may never return to 2023 levels. The structural reallocation toward AI infrastructure represents a permanent shift in manufacturing priorities.

If you need storage, buy now. Every forecast predicts additional 20-40% increases through Q2 2026. The 1TB drive that costs $130 today may cost $180 in three months. Waiting will likely cost more, not less.

Micron, Crucial’s parent company, announced in December 2025 that it’s exiting the consumer memory market entirely to focus on enterprise and AI customers. The Crucial brand will be wound down, with remaining inventory being sold at premium prices.

Yes, significantly. HDDs cost approximately $15-18 per TB versus $100-130+ per TB for SSDs—a 7-8x gap, the widest since 2019. However, HDDs are also experiencing shortages with enterprise drives backordered 52+ weeks.

AI accelerators require High Bandwidth Memory (HBM), which consumes 3x the wafer capacity per GB compared to standard memory. Projects like OpenAI’s Stargate require 40% of global DRAM output. Every wafer allocated to AI is a wafer denied to consumer SSDs.

According to Kingston, NAND prices have increased 246% since Q1 2025, with 70% of that increase occurring in just the last 60 days. The same 1TB TLC chip that cost $4.80 in July 2025 now costs $10.70.

4TB and 8TB drives currently offer the best $/TB value. Enterprise demand focuses on maximum capacity, leaving these mid-range consumer capacities relatively better supplied. Smaller capacities (500GB-1TB) have experienced larger percentage increases.

Related Resources

- Seagate IronWolf NAS Drives — For hybrid storage solutions

- IronWolf 12TB — Best $/TB in NAS drives

- IronWolf Synology Compatibility

- IronWolf 525 NVMe — NAS SSD caching

- IronWolf vs Exos — Enterprise HDD comparison

- RAID Calculator — Plan your storage configuration

Last Updated: February 2026

Sources: Tom’s Hardware, TrendForce, IDC, Wikipedia (2024-2026 Global Memory Supply Shortage), company earnings calls and press releases, analyst reports from Morgan Stanley, Goldman Sachs, and Bank of America.